AI Reshapes Europe’s Digital Payments and E-Commerce in 2025, but Challenges Remain

By 2025, artificial intelligence is increasingly central to Europe’s evolving digital payments and E-Commerce ecosystems. Companies across the continent are embracing AI to boost efficiency, align with regulations, and unlock innovative use cases. Yet this momentum is offset by barriers such as fragmented infrastructure, skill shortages, and public skepticism. As adoption grows, differences in readiness and scalability shape how AI is applied across markets.

AI Powers Efficiency and Personalization Across Payments and E-Commerce

AI is accelerating transformation across Europe’s financial and commercial systems. Companies are embedding AI in business functions, from backend automation to fraud protection and customer interaction, streamlining operations and personalizing user experiences.

In payments, AI automates customer onboarding, credit decisions, and compliance. Startups like Arva AI and Intuitech simplify financial workflows, while institutions modernize legacy systems via platforms like Tweezr. AI’s role in fraud prevention is vital, improving real-time detection of suspicious activity.

In E-Commerce, firms like LVMH use AI for branding, streamlined operations, and personalized experiences. AI-generated mood boards support product design, semantic search enhances conversions, and embedded agents help sales teams with follow-up outreach. These tools are especially valuable in today’s cautious spending environment.

AI also transforms embedded finance for SMEs. Merchant cash advance models have grown by 50%, per Oliver Wyman, as AI assesses borrower risk, analyzes sales data, and forecasts repayment, allowing PSPs and fintechs to offer embedded financing through online and point-of-sale platforms.

Regulatory Standards Establish Guardrails for AI Deployment

Europe’s layered regulatory environment comprising the AI Act, GDPR, and DORA guides AI deployment in commerce and finance. These frameworks enforce compliance, transparency, and ethics in high-risk areas such as biometric security and automated customer service.

DORA mandates ICT risk management protocols for financial institutions. Transparency rules under the AI Act and BaFin require companies to inform users of AI interactions. Cross-border firms face hurdles in aligning operations with EU standards.

Voluntary initiatives such as the AI Pact and national sandboxes help companies preempt formal enforcement by piloting AI technologies and refining protocols in controlled environments.

Public Trust and Workforce Gaps Slow AI Integration

Despite growing enterprise use, public trust in AI remains modest. As of January 2025, no surveyed market exceeds 54% in trust, with Spain leading at just over 40%. Estonia, Latvia, and Switzerland follow, while Finland, Belgium, and the Netherlands report lower confidence, according to KPMG and The University of Melbourne.

Workplace adoption peaks at 54% in some countries, but general trust hovers between 39% and 55%. Switzerland and Norway are exceptions, with strong adoption and trust coexisting highlighting Europe’s uneven confidence landscape.

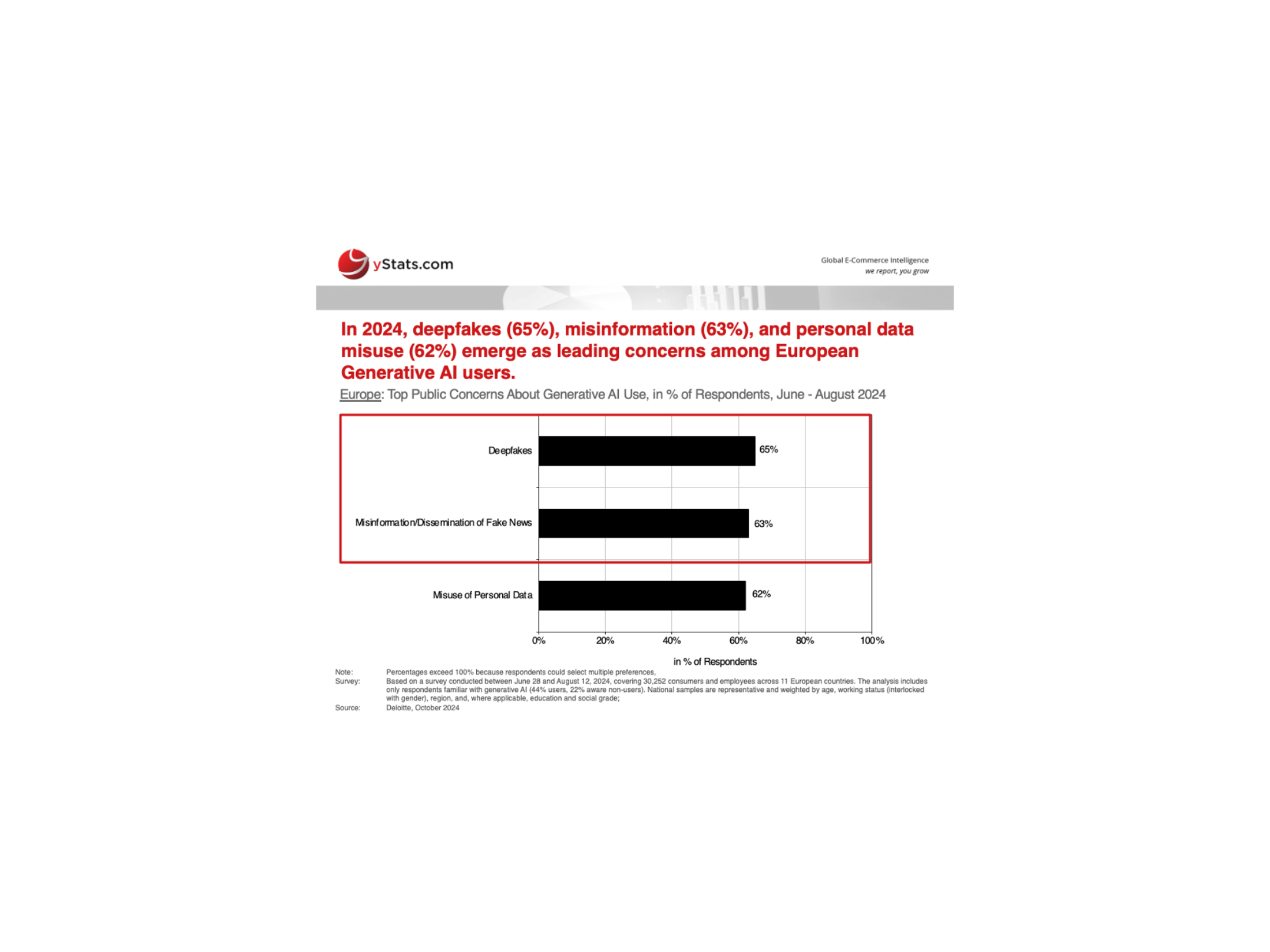

Generative AI intensifies concerns. Deloitte finds over 60% of Europeans worry about deepfakes and data misuse. Risks like onboarding manipulation and identity spoofing complicate compliance, prompting regulators such as the EBA to warn about transparency and ICT vulnerabilities in customer-facing AI systems.

Beyond trust, talent shortages constrain scalability. McKinsey notes fewer than 15% of top AI researchers are trained in Europe, where developers also earn less than in the U.S. Weak investment in reskilling and infrastructure further limits Europe’s global competitiveness.

Different National Strategies Reflect Divergent Maturity Levels

National approaches to AI vary widely. In Germany, nearly 70% of companies have adopted GenAI strategies, though ethics and compliance concerns persist, as per KPMG. France emphasizes productivity but struggles with talent shortages. Spain leads in AI agent deployment, supported by trust and tech investment.

Nordic countries take a cautious approach, slowed by regulatory ambiguity and limited executive engagement. Executives fear legal missteps, curbing AI exploration. Poland faces structural limits, including lack of strategy and low SME participation, despite enthusiasm from large firms. These divergent strategies underscore the fragmented pace of operational maturity across the region.

Europe Trails in Infrastructure, Funding, and Model Development

Europe lags globally in foundational AI capabilities. McKinsey reports competitiveness in only half of the eight core GenAI value chain segments. Gaps remain in semiconductor production, cloud services, and computing power. Only 25 of 101 major foundation models are European, and under 15% of global AI SaaS investment reaches the region. AI workloads could increase electricity use by over 5% by 2030, pressuring energy infrastructure. Without upgrades, AI scaling may stall.

The EU’s AI Continent Action Plan commits EUR 20 billion annually to AI through 2030. Complementary efforts like AI Factories and the AI Skills Academy aim to enhance innovation and reduce reliance on U.S. providers by promoting open-source solutions and public-private partnerships.

AI Enhances Emerging Payment Infrastructure and Open Banking

AI also strengthens next-gen financial services. The ECB’s digital euro project could standardize payments and introduce AI-based fraud analytics and behavior tracking. Cross-border interoperability and shared standards will be critical to success.

In open banking, intelligent tools like real-time balance validation and dynamic discounts are making progress. Though uptake is modest, these innovations enhance safety and functionality, positioning open banking as a viable card alternative.

Together, these developments position AI as a strategic driver of modernization—not just optimization.

Strategic Collaboration Needed to Close the Gap

By 2025, AI improves fraud detection, personalization, and access in Europe’s payment and E-Commerce sectors. But systemic challenges in trust, talent, infrastructure, and policy remain.

To close the competitiveness gap and achieve digital sovereignty, Europe must align investments, workforce development, and regulation. Only coordinated action will unlock AI’s full potential across its digital economy.